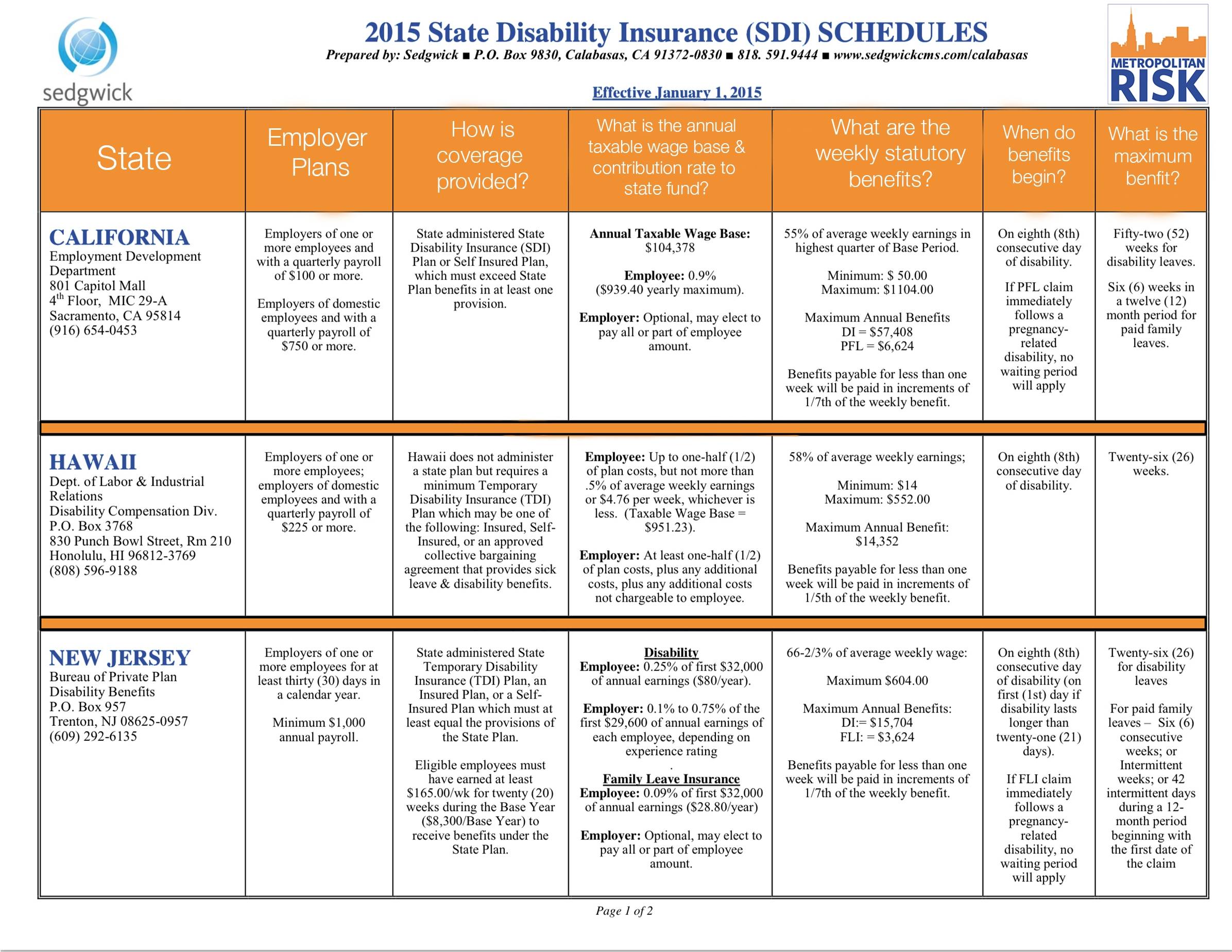

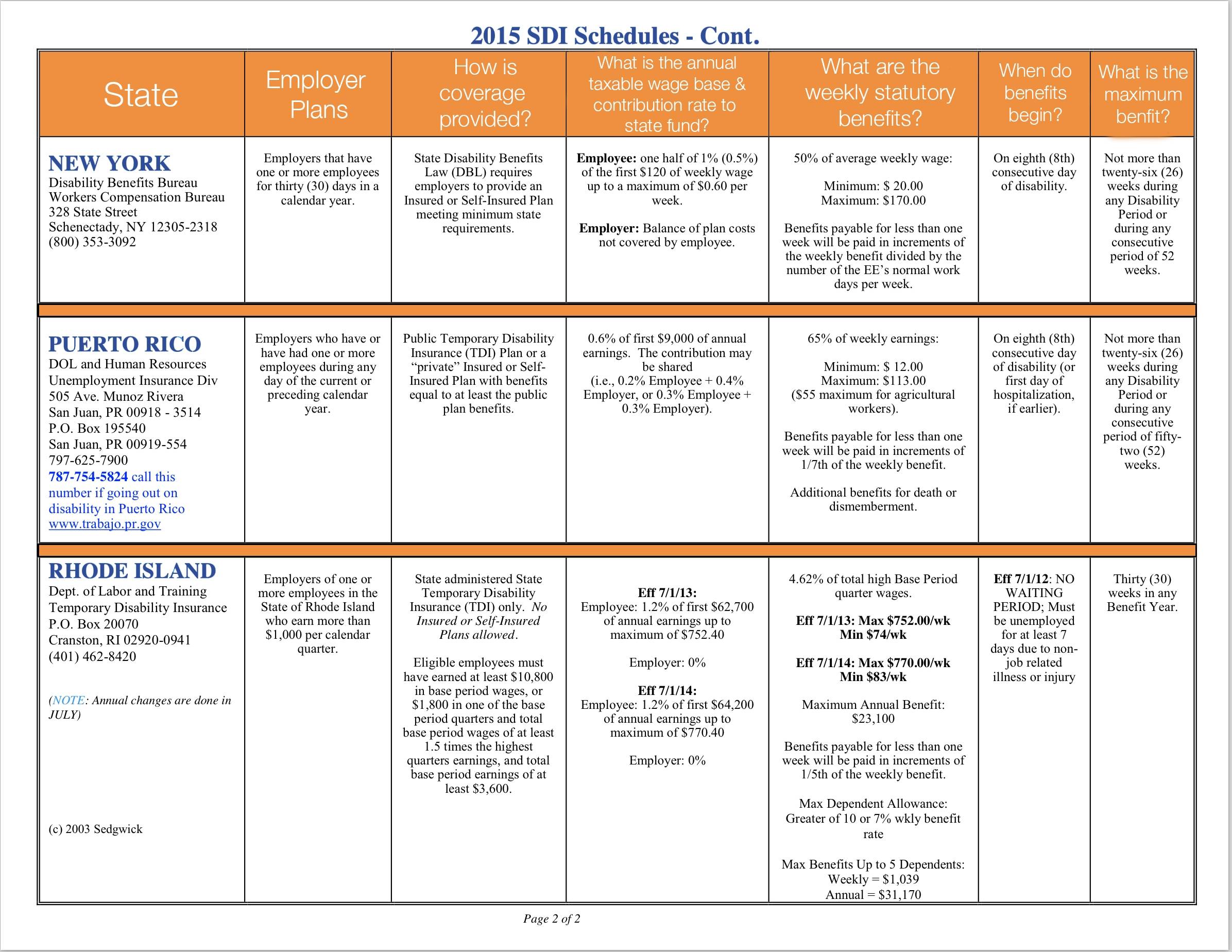

In New York, Short Term disability is an employer required program that pays 50% of pre-disability wages, up to a maximum of $170.00 per week (unless the employer provides additional coverage) to an employee who is unable to work, because of any injury or illness, which did not occur on the job or while performing work related duties, which now prevents the employee from performing their regular job.

Eligibility requirements vary slightly by policy but generally, the requirements are:

The illness or injury must be non-work related – Short term disability applies to injury and illness suffered outside of work related environment and/or work related activities. Ex: non work related cancer, liver disease, injury sustained at home non work related , flu, pregnancy, diabetes, etc.

Service Wait period – This states the employee must be an active employee for a set time-period prior to being eligible for short-term disability benefits. For example, Mary is looking to collect disability. According to her company-sponsored plan, Mary has to be employed by her company for at least 30 days prior to her becoming disabled in order to be eligible. This should be written within the Employee Manual.

Benefit Wait period – There is a one-week waiting period before benefits are payable. Benefits commence on the 8th day of disability. Benefits are not issued retroactively, to include the 7 days waiting period.

Policy Specifc Requirements

There are some additional criteria that are dictated by the employer’s individual policy, which are also considered prior to adjudicating a disability claim:

- Full time employment versus part time employment – some policies offer benefits to part time employees while other restrict benefits to full time employees, only.

- Use of vacation time – Check the policy language to determine if employees are required to use vacation or sick time, prior to commencement of disability benefits.

- Pre-existing conditions are health issues that existed before applying for health insurance. Most common are 3/12 pre-ex provisions; the employee must be actively employed for at least 12 months with no treatment 3 months prior to eligibility date for said disabling condition. The employer should be aware of this provision but does not have to look into it with great detail. The carrier will make the determination to deny based on this provision; it is not the responsibility of the employer.

Reporting

A typical disability claim requires the following:

- Form DB 450

- The employee completes Part A

- The physician completes Part B

- The employer completes Part C

Completed claim forms are then filed with the insurance carrier either by fax, email or mail. Check with your disability carrier on ways to file the claim.

* If you are a client of Metropolitan Risk just file the claim on our website and upload the form. We do the rest.

***Note: Claims can be reported no sooner than 30 days prior to disability. This also applies to pregnancy claims. The carrier will deny a claim if it is filed too soon. If that happens, the application process will have to be performed all over again.

Benefits

Duration: Benefits last no more than 26 weeks. Once the employee has exhausted 26 weeks of benefits, the claim will transition to Long-term disability, for which a separate application is sent, directly to the employee by the carrier.

Frequency: Benefits are paid weekly within the 26 weeks period.

Amount: Benefits are 50% of the pre-disability earnings, but no more than the maximum benefit allowed, currently $170 per week (NY max).

Taxes: Disability income from a disability-insurance policy can be taxable depending on how the premiums were paid, i.e. “pre-tax or post tax.” Contact the disability administrator for details.

For any questions about the provisions in your disability policy always contact your disability administrator, or download our Workers Comp Coverage Checklist to contact a Risk Advisor if you have additional questions.